Blog

Architecting the intelligent auto lender: A roadmap to agentic AI

By Bilal Arif Deputy Director Global Marketing, on October 31, 2025

Discover how agentic AI transforms auto finance, enabling faster credit decisions, compliance, and lifecycle automation through autonomous agent ecosystems.

Table of Contents

Share this Blog:

Introduction: Why agentic AI matters

Auto finance is under growing pressure to deliver faster approvals, transparent risk decisions, and personalized experiences without compromising compliance. Agentic AI offers a practical pathway to that equilibrium. Agentic artificial intelligence describes AI systems that can perceive context, reason about objectives, act autonomously, and improve over time. Research from Boston Consulting Group predicts that multi‑agent systems could deliver US$53 billion in business value by 2030, up from US$5.7 billion in 2024. These systems are already contributing meaningfully to enterprise value: BCG’s 2025 AI report estimates that agents account for 17 % of total AI value today and could rise to 29 % by 2028. For auto finance companies, whose core activities revolve around credit assessment, customer engagement, and compliance, the progression from simple automation to autonomous ecosystems offers a path to efficiency, differentiation, and new revenue models. The model below illustrates this progression in an auto-finance context, showing how lenders can move from isolated automation pilots to interconnected, self-improving agent ecosystems that coordinate underwriting, fraud, servicing, and dealer collaboration in real time.

For a practical discussion of when and how auto and equipment finance lenders should actually deploy AI, including which use cases deliver the clearest ROI, the webinar AI deployment in auto finance covers the decision framework and implementation priorities that leaders across the sector are using.

Stage 1: Assisted automation

At the base of the agentic AI journey are assistants that follow predefined rules. In auto finance, this stage includes chatbots answering loan queries, RPA bots orchestrating document collection from predefined sources, and digital schedulers booking test drives. These systems follow predefined scripts and cannot adapt to new contexts or learn from outcomes. Their role is to reduce manual effort by handling repetitive, low-judgment workflows. A Mckinsey survey reports that 78% of organizations use AI in at least one business function. Financial services invested roughly US$35 billion in AI in 2023, indicating widespread use of basic automation. However, most projects remain pilots; only 26% of companies feel ready to scale AI beyond proof-of-concept. These early tools deliver efficiency but offer limited autonomy and are constrained by existing legacy systems and siloed data.

How it works

Single-action automation operating in one direction. No independent decision-making. No feedback loop.

Examples

- Chatbots answering basic loan questions

- Automated document reminders & notifications

- Form pre-fill & data extraction macros

- Routing support tickets to the right team

- Outcome

Improved speed and reduced manual workload, but limited intelligence and adaptability.

Stage 2: Autonomous task agents

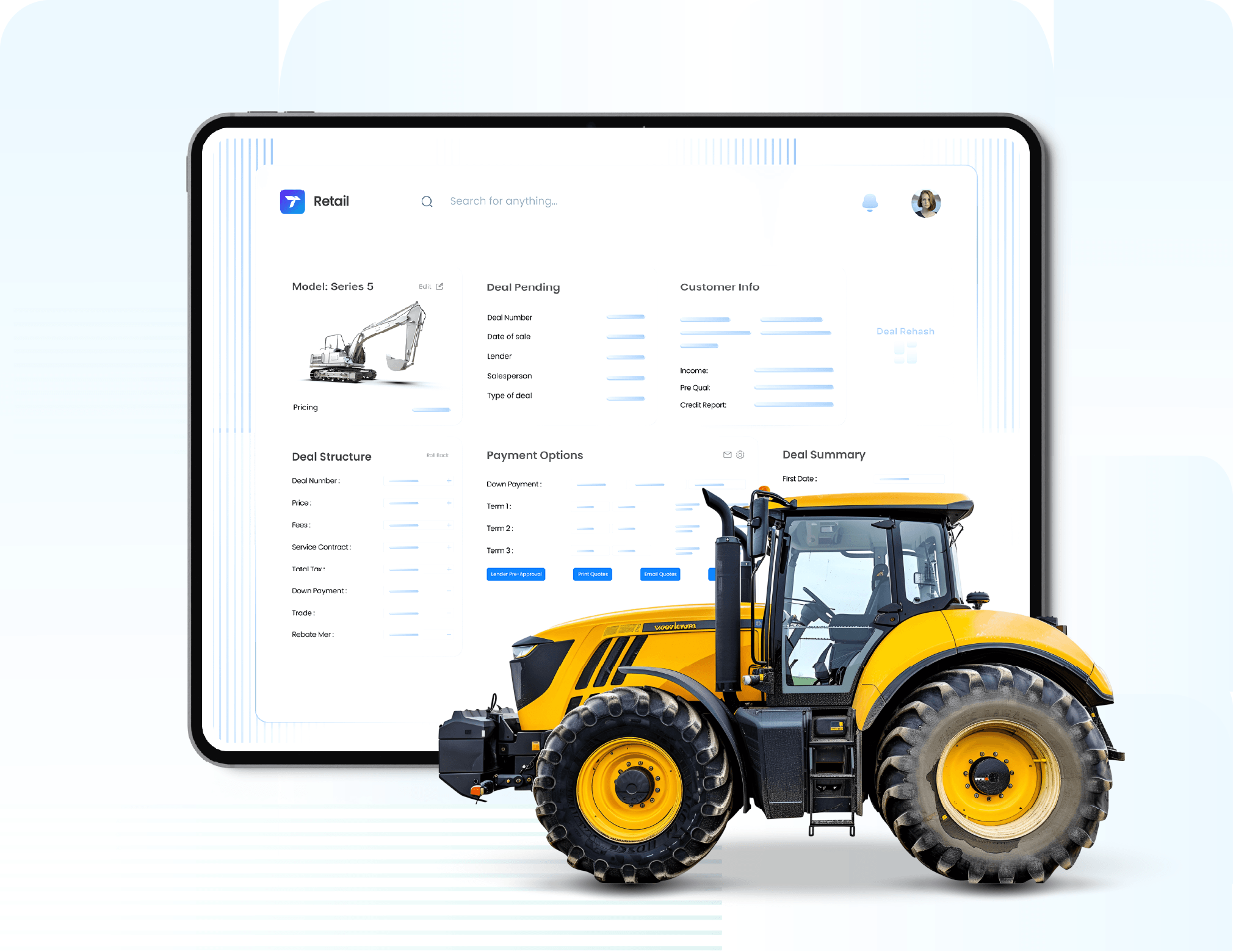

Task-focused AI agents execute multi-step journeys with context and reasoning. They can ingest structured and unstructured data, evaluate multiple inputs, and complete processes end-to-end autonomously within a defined scope. These agents are not merely executing scripts; they analyze credit variables, fraud signals, documents, and historical outcomes to recommend or finalize decisions. Feedback loops allow the model to refine outputs over time under governance supervision.

In auto finance, underwriting is the prime candidate. Traditional underwriting depends on manual data collection and rigid rules. NETSOL’s Check AI illustrates a simple agent approach: it acts as an AI‑native credit decisioning engine that gathers data from multiple sources, processes documents, and performs financial analysis. It uses reasoning-driven ML models and workflow orchestration to interpret information and generate structured credit insights. Critically, it includes a human‑in‑the‑loop design, allowing analysts to review and refine decisions. Such specialized agents can dramatically accelerate processes; an analytics study noted that AI can reduce credit approval cycles by up to 60 %.

How it works

Multi-step intelligent execution within a bounded domain. Input → reasoning → verdict or action.

Examples

- Automated underwriting & pricing suggestions

- Income, employment, and identity verification

- AI-based fraud & anomaly detection

- Contract review & compliance checks

Outcome

Faster, more accurate credit and risk decisions with humans still supervising edge cases.

Stage 3: Multi-agent orchestration

At this stage, multiple specialist agents work together like cross-functional digital teammates. Each agent performs its own task while ensuring seamless workflow movement. Deloitte explains that such multi‑agent systems can autonomously orchestrate tasks such as Know Your Customer (KYC) maintenance: one agent pulls public data, another assesses risk, and a third files regulatory updates without human handoffs. For auto finance companies, collaborative agents can coordinate identity verification, risk scoring, fraud detection, and pricing. Instead of isolated decision workflows, intelligence becomes coordinated across systems. These agent teams reduce hand-offs, accelerate approval cycles, and create unified audit trails, making them ideal for regulated lending environments.

The blog on beyond LLMs examines this evolution in depth, how the industry is moving from large language models as standalone tools toward orchestrated, agentic systems that can reason, act, and improve across interconnected workflows.

How it works

Distributed decision-making. Agents share context and coordinate their outputs to achieve a single objective.

Examples

- One agent validates identity

- Another analyzes bank statements

- Another monitors fraud signals

- Another confirms inventory and deal structure

- Unified decision delivered to lender & dealer

Outcome

Streamlined decisioning across departments, improved compliance, and lower fraud exposure.

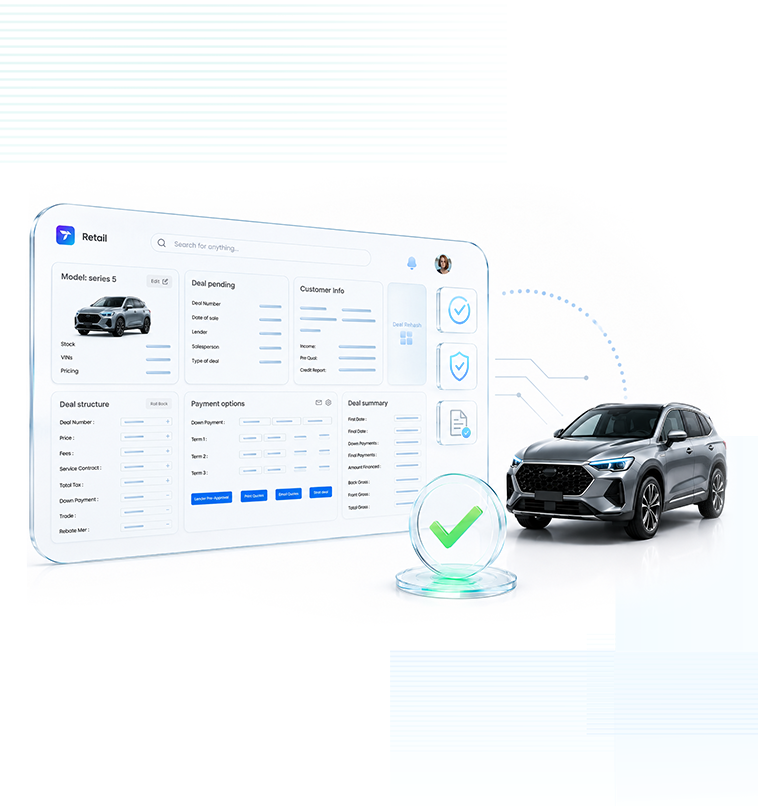

Stage 4: Integrated agentic AI ecosystems

This is the frontier: interconnected, self-optimizing agent networks orchestrating the entire auto-lending lifecycle from lead qualification to funding, servicing, renewals, and remarketing. Instead of automating tasks or workflows, the ecosystem continuously learns, adapts, and optimizes operations in real time. In auto finance, agent ecosystems could handle the entire lifecycle: digital retail agents guide consumers from vehicle selection through financing; underwriting agents collaborate with KYC, fraud, and pricing agents; servicing agents manage payments and refinancing; and orchestration agents coordinate interactions among lenders, dealers, OEMs, insurers, and charging networks. Such transformation requires significant process redesign and governance, as legacy systems and immature standards impede integration. Yet the potential value is immense. KPMG estimates that agentic AI could unlock US$3 trillion in global productivity gains.

How it works

Distributed, goal-aligned intelligence across interconnected systems, partners, and channels, continuously improving outcomes.

Examples

- Unified agent network coordinating lenders, dealers, OEMs, and third-party data providers

- Dynamic loan pricing based on risk shifts, market signals, and vehicle data

- Proactive compliance & real-time audit controls

- Predictive servicing, early delinquency intervention, and retention recommendations

Outcome

A self-learning auto-finance operating system enabling faster decisions, lower risk, higher recovery, and superior customer experience across the full lifecycle.

Strategic considerations for each stage

Modernize infrastructure: Agentic AI thrives in connected, API‑first environments. Deloitte stresses that legacy integration is a significant barrier. Investing in cloud‑native, microservices‑based platforms enables agents to access and share data seamlessly. Transcend Finance’s end-to-end automotive finance platform and API-first architecture exemplify the foundational technology required to enable agentic AI at scale.

Prioritize high‑impact use cases: To progress beyond AI assistants, firms should select use cases with clear ROI. Underwriting and KYC deliver measurable benefits, with studies showing substantial reductions in approval times and losses. Fraud detection and dynamic pricing are natural candidates for collaborative agents.

Build cross‑functional teams: A lack of technical expertise is a common barrier. Auto finance companies need cross‑functional teams spanning data science, risk management, legal, and operations to design, deploy, and govern agentic systems. Continuous training ensures that staff can oversee and collaborate with autonomous agents.

Ensure interoperability: Agentic systems need seamless connectivity between legacy platforms and modern AI components. Establishing standard data formats and shared communication protocols enables secure, consistent data exchange across lenders, OEMs, and fintech partners, ensuring every part of the ecosystem can operate as one.

Embed governance and ethics: As autonomy increases, so do risks. Human oversight remains essential. KPMG emphasizes the importance of categorizing agents and establishing guardrails.

Preparing for the future of auto finance

The evolution from rule‑based assistants to autonomous agent ecosystems is reshaping the auto finance industry. Early steps bring efficiency gains, while later stages promise end‑to‑end orchestration and new business models. Companies that modernize their infrastructure, focus on high‑value use cases, build cross‑disciplinary teams, and implement robust governance will be best positioned to harness agentic AI. As multi‑agent capabilities expand, auto finance firms have an opportunity to reimagine the entire vehicle finance experience, delivering faster decisions, better customer engagement, and integrated mobility solutions.

For auto finance leaders building out their AI strategy, the whitepaper AI roadmap for auto finance leaders, provides a five-step framework for moving from AI pressure to measurable performance, covering infrastructure investment, use case prioritisation, governance, and the organisational changes required to scale agentic AI responsibly.

Start building your path to agentic AI today. Partner with NETSOL to design, deploy, and scale intelligent systems that drive real business impact across the entire auto finance lifecycle.

Related blogs

Blog

Equipment finance software has to hold a schedule and a meter

Blog

Automotive digital retailing only works if the desk can close the deal

Blog