Blog

Connected decision flows: The new baseline in auto retail

By NETSOL Technologies , on October 28, 2025

Discover how connected decision flows replace fragmented auto retail processes, AI-assisted approvals, consistent risk execution, and higher deal conversion rates.

Table of Contents

Share this Blog:

The shift is structural, not hypothetical

Auto digital retail is not waiting for fully autonomous AI underwriting to transform the market. The shift is already happening. It is driven by the move away from manual, fragmented approval processes toward connected decision flows that remove handoffs, shorten cycle time, and enforce uniform execution. These flows are increasingly powered by AI-assisted decisioning that interprets data, applies policy, and recommends next actions in real time, turning static processes into adaptive systems. In a market where hesitation and delay directly translate into lost deals, this evolution is structural.

Furthermore, McKinsey reports that nearly one in three U.S. buyers now plan to complete their next vehicle purchase fully online, and nearly one in four prefer a hybrid path that starts online and finishes in-store. This reinforces the need for connected decision flows that do not reset when the channel changes.

But why is this shift in motion?

Manual finance execution is no longer defensible

The historical approach to credit decisions was built for a slower buyer. Multiple systems, manual touchpoints, separate credit pulls, spreadsheet checks, and static rule engines were tolerable when customers expected to wait. That expectation is gone.

Fragmented decisioning creates three visible outcomes:

- Delay turns into hesitation

- Hesitation turns into abandonment

- Abandonment turns into permanent loss to competing channels

This is a commercial and cost problem as much as it is a customer experience issue.

Industry analysts covering NADA 2025 observed that removing legacy bottlenecks in inspection, trade-in, contracting, and approval flows can produce profit uplifts approaching 20% without increasing volume. The economics are coming from workflow correction, not growth.

Fragmentation, not judgment quality, is the real bottleneck

Most inefficiency in auto finance and retail does not come from poor credit policy. It comes from disconnected execution. When credit bureaus, CRM, pricing, desking, fraud checks, and contracting live in separate lanes, every deal is manually reconstructed by staff. AI-assisted, connected decision flows eliminate this reconstruction work by allowing validation, pricing, approval, and contracting to run in a continuous loop rather than being recreated at each step. AI-driven orchestration continuously aligns data from CRM, lenders, and fraud engines, ensuring that every step in the financing journey inherits verified inputs instead of re-collecting or revalidating them.

The webinar retail gap "What Dealers Really Want from Digital Retailing" examines these execution friction points from the dealer's perspective, exploring the disconnect between what digital retail technology promises and what dealerships actually experience when systems don't connect cleanly.

The operational impact is immediate. Fewer touches. Fewer inconsistencies. Minutes instead of hours.

Uniformity is now as valuable as speed

Speed is the visible benefit, but uniformity is the strategic one. Fragmented decisioning produces inconsistent outcomes for similar risk. It also produces channel-dependent approvals, uncontrolled pricing erosion, and risk drift across the portfolio. Connected decision flows apply one execution model across all channels. The rules and controls travel with the deal instead of relying on individual interpretation.

Automation protects human capital instead of replacing it

According to an industry article, when data ingestion is automated in auto finance operations it can save 30–40% of hours previously spent on manual data entry.

AI-assisted decisioning redefines automation in retail finance. It doesn’t remove analysts; it refocuses them. They ensure analysts are used only where needed. Routine and standard cases are processed systemically. Edge cases and high-risk profiles are escalated to human review. This protects the margin on both sides.

Cost of labor falls because routine volume no longer consumes specialist time. Risk quality improves because experts do not waste attention on low-variance files.

The commercial upside is the consequence, not the thesis

Once delay and inconsistency are removed, conversion improves. When customers move from inquiry to contracting without stalls, they stay in the funnel. When decisions are delivered in minutes, sales teams can close instead of babysitting the process.

The improvement in revenue, personalization in customer service, and deal completion rate is a downstream effect of operational correction, not the primary argument.

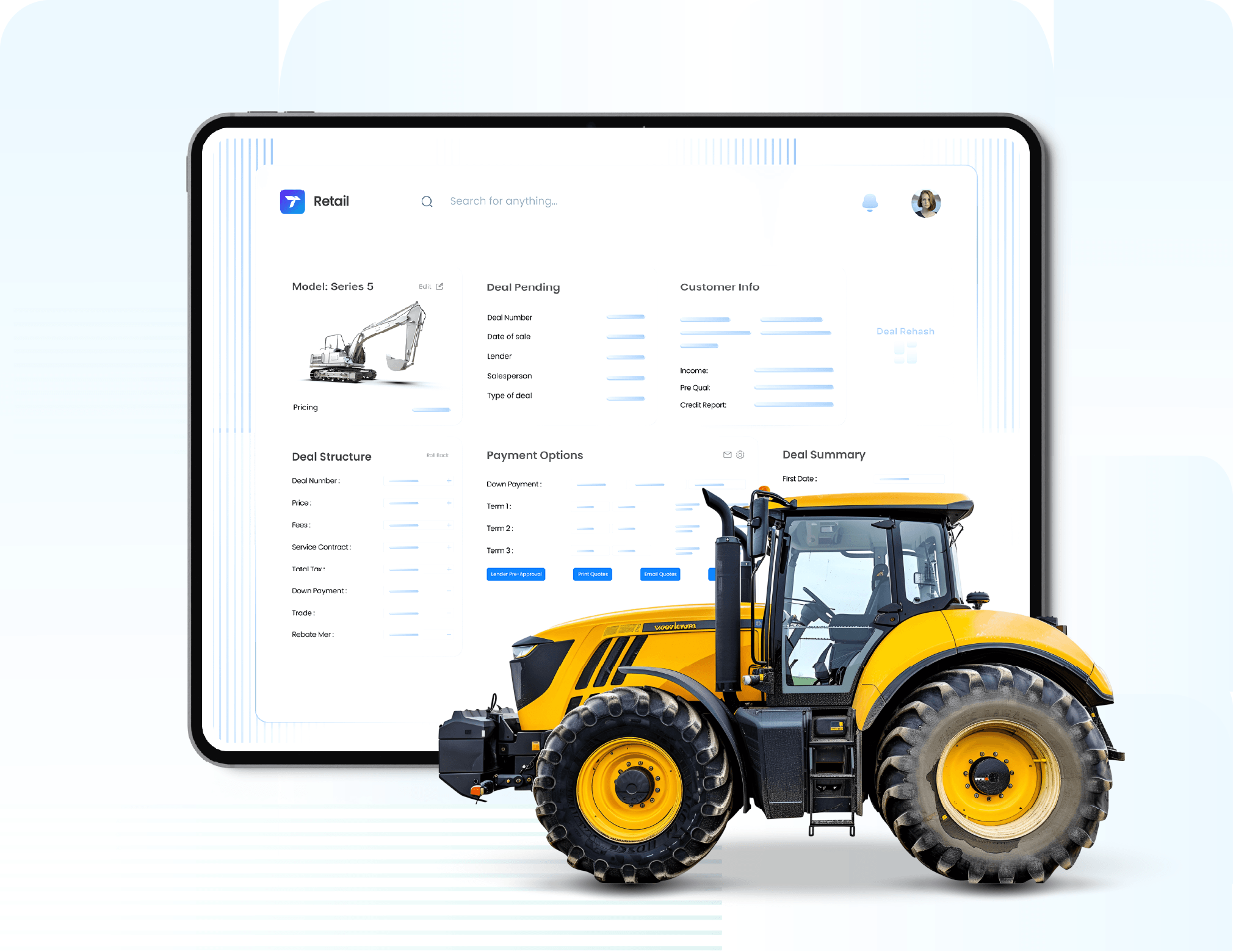

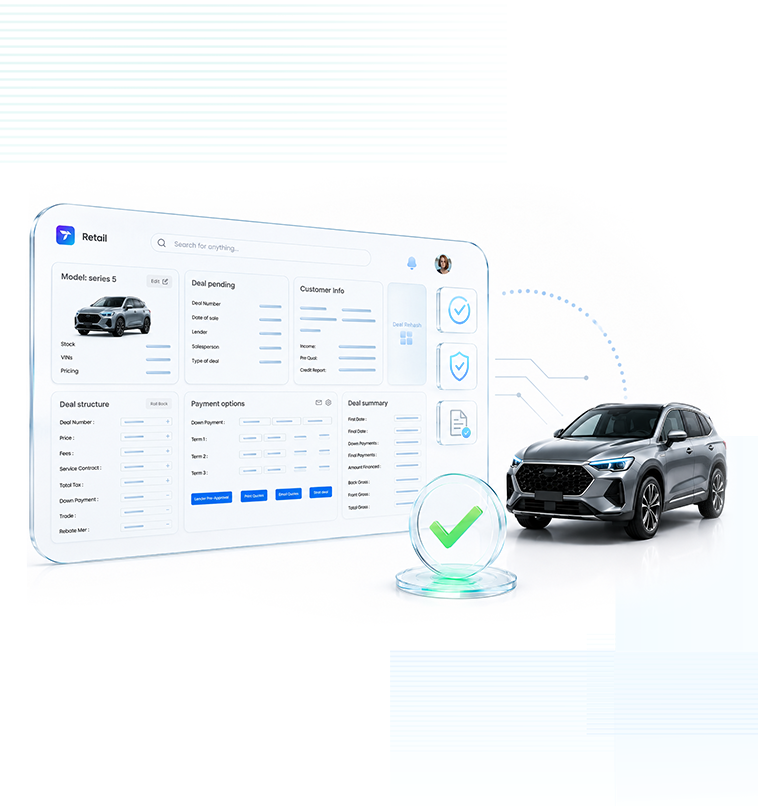

Platforms are becoming the standard execution layer

U.S. dealers, captives, and OEM retail programs are not building their own orchestration stacks. They are adopting platforms that already integrate financing, desking, fraud prevention, multi-lender credit submission, automated credit decisioning, and digital contracting into a single, controlled workflow.

Modern retail platforms are embedding AI-assisted decision layers to govern each transaction path, ensuring consistent interpretation of data and policy without adding complexity to the dealer’s workflow.

Transcend Retail is an example of this operating model in the market, with connected decision flows spanning auto retail last mile and dealership back-office execution, including automated credit decisioning, contracting, ID verification, and trade-in within a single flow.

The baseline has shifted

In prior cycles, speed and digital retail were differentiators. In the current U.S. auto retail environment, connected decision flows, powered by AI, are the new baseline for competitiveness. Manual, siloed, and approval-driven retail finance is no longer just inefficient. It is structurally uncompetitive against lenders and retail models that move with continuity and precision.

The organizations that treat connected decision flows as infrastructure, not as a feature, will control the next phase of margin, trust, and throughput in auto retail finance.

For OEMs, captives, and dealer groups building the architecture that makes connected decision flows scalable, the whitepaper auto captive stack provides the blueprint for an AI-first, API-connected, composable platform structure, the technical foundation that turns connected execution from a feature into operating infrastructure.

Related blogs

Blog

Equipment finance software has to hold a schedule and a meter

Blog

Automotive digital retailing only works if the desk can close the deal

Blog