Blog

From credit checks to credit intelligence: AI underwriting for auto captives

By NETSOL Technologies , on February 27, 2026

Learn how NETSOL Check transforms traditional credit assessment into intelligent, efficient decision-making for better portfolio management and faster growth.

Table of Contents

Share this Blog:

Captive finance organizations are under more pressure today than at any point in the past decade. On one hand, OEMs expect faster approvals, higher conversion rates, and seamless dealer experiences. On the other hand, regulators demand transparency, explainability, and stronger governance across credit decisions.

This creates a critical paradox. Captives must move faster while becoming more compliant and risk-aware at the same time.

Yet many underwriting environments are still built on legacy credit check models, manual reviews, and fragmented data systems. While digital retail, API ecosystems, and AI-led customer journeys are advancing rapidly, underwriting often remains one of the slowest and most operationally heavy functions within the automotive lending software stack. This gap is not just operational; it is strategic.

The current underwriting challenges captives are facing

To understand the shift toward credit intelligence, it is essential to first examine the structural issues shaping captive underwriting today.

1. Fragmented data across disconnected systems

Many captives operate with data spread across origination, dealer systems, credit bureaus, and internal risk platforms. This fragmentation leads to:

- Manual data reconciliation

- Inconsistent risk views

- Delayed credit memos

- Limited predictive insights

For a broader view of how agentic AI is addressing exactly these underwriting inefficiencies and how captives can move from isolated automation to interconnected decisioning, the blog on intelligent auto lender architecture maps the full progression from simple rules-based tools to AI agent ecosystems in auto finance.

Valuable financial data often sits in silos and is reconciled manually instead of being continuously analyzed for intelligence-driven decisioning.

2. Slow and manual credit decision cycles

Traditional underwriting processes rely heavily on document reviews, manual memo drafting, and repetitive validation tasks.

Typical legacy underwriting workflow

3. Rising regulatory and compliance pressure

Captives are increasingly required to justify credit decisions with audit-ready documentation and explainable risk frameworks. However, legacy systems often lack:

- Traceable decision logic

- Versioned policy enforcement

- Explainable outputs

NETSOL's United Trust Bank case study demonstrates how a regulated lending institution has built technology infrastructure that satisfies exactly these audit-ready and explainability requirements, across credit origination, servicing, and reporting within a complex compliance environment.

As underwriting grows more complex, the absence of auditable intelligence increases compliance risk and operational strain on credit teams.

4. Inability to operationalize the 5 Cs of Credit at scale

The traditional 5 Cs of Credit (Character, Capacity, Capital, Collateral, Conditions) remain foundational, but in many organizations, they are still applied manually.

This results in:

- Analyst bias

- Inconsistent evaluations

- Limited standardization

- Difficulty scaling across markets

Modern captive environments require these principles to be digitized into structured, auditable workflows rather than subjective assessments.

5. Experimentation paralysis due to legacy cores

Even minor policy updates or workflow changes in traditional underwriting stacks can require extensive regression testing. This slows innovation and prevents captives from adapting quickly to evolving risk models, customer behavior, and market shifts.

Why traditional credit checks are no longer enough

Credit checks provide a static snapshot of borrower risk.

But today’s mobility finance ecosystem is dynamic.

Customers have evolving income streams, new ownership models are emerging, and asset values (especially EVs) fluctuate more frequently. Static credit evaluations cannot capture these real-time signals effectively.

The shift toward credit intelligence in captive ecosystems

Forward-looking captives are now embedding AI into underwriting workflows to transform decisioning from manual assessment to contextual intelligence.

An AI-powered underwriting approach enables:

- Real-time financial data extraction

- Automated validation and structuring

- Contextual risk signal analysis

- Standardized credit memoranda generation

Instead of replacing analysts, this model enhances human judgment by providing structured insights and stronger decision-making starting points.

Reframing underwriting as a strategic growth function

Underwriting is no longer a back-office control layer. It directly impacts dealer satisfaction, customer experience, conversion rates, and portfolio quality.

As consumer loyalty declines and digital-native lenders offer faster approvals, captives must deliver seamless and intelligent credit journeys to remain competitive.

How intelligent underwriting addresses core captive pain points

1. Operational Efficiency

Automation of data preparation, document review, and memo drafting frees analysts from repetitive tasks and improves productivity.

2. Faster, audit-ready decisions

Natural-language policies can be converted into executable and auditable rules, ensuring consistent and traceable credit decisions.

3. Enhanced governance and compliance

Clear oversight and decision monitoring strengthen model risk management and fair-lending compliance, without slowing approvals.

4. Analyst foresight and contextual intelligence

Richer insights empower credit teams with clearer risk perspectives and optimized loan structuring capabilities.

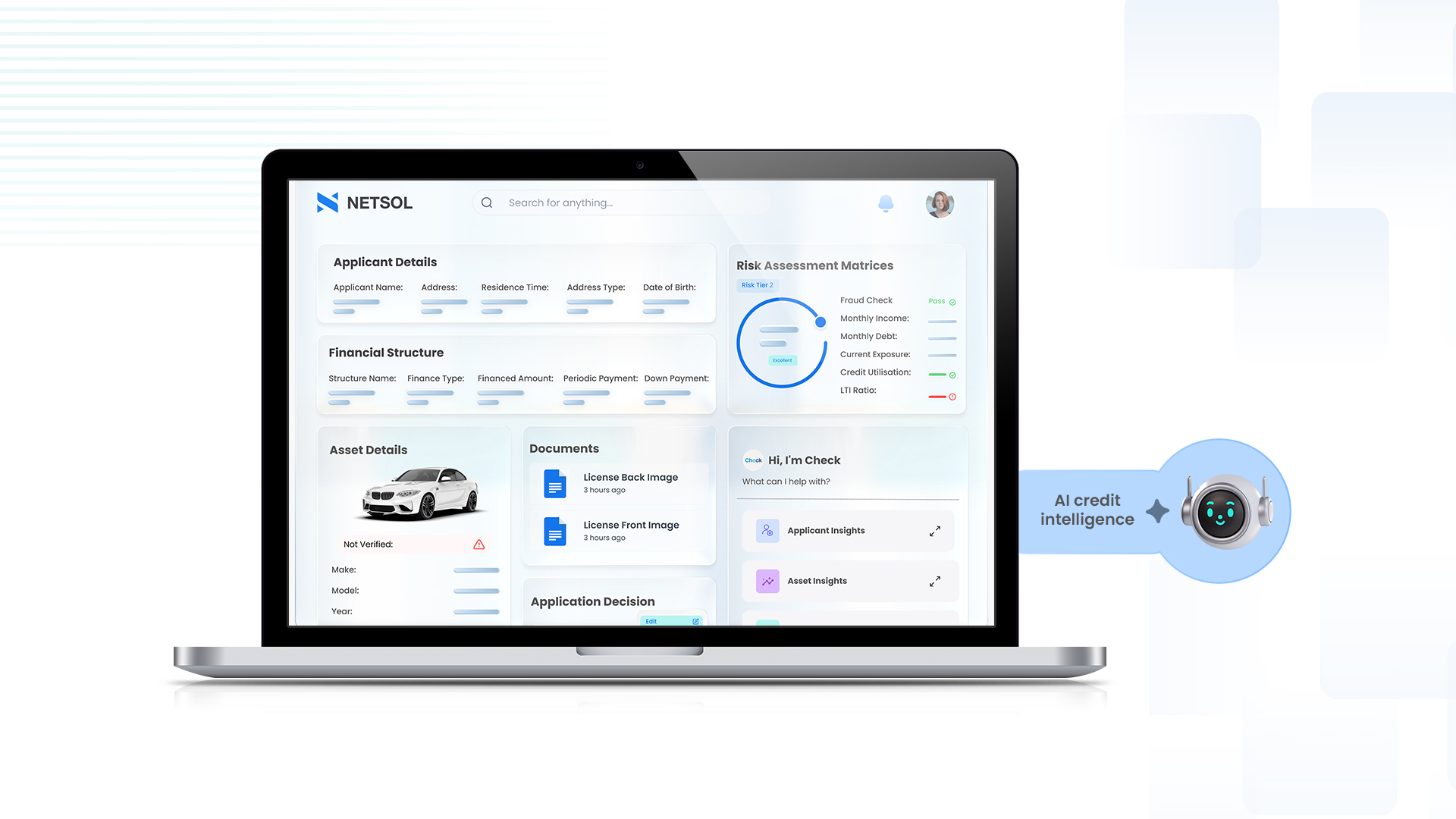

Check powered by Transcend Marketplace

As captives transition from manual credit checks to intelligent decisioning, solutions purpose-built for AI-powered underwriting are becoming essential.

NETSOL Check, part of Transcend AI Labs, is designed specifically to address the structural underwriting challenges captives face today. Rather than overhauling existing core systems, it streamlines credit assessment by embedding intelligence into the decision workflow. Built as an AI-native solution on the Transcend Finance platform, Check AI draws on generative AI capabilities to combine deep reasoning, intelligent automation, and agentic workflows to turn data into actionable credit decisions in real time, full details are in the Check AI launch announcement.

Conclusion

The challenges facing captive finance underwriting are no longer isolated operational issues; they are strategic barriers to growth, agility, and customer experience. Fragmented data, manual workflows, regulatory pressure, and static credit checks are collectively slowing down decision cycles in an increasingly real-time finance ecosystem.

The shift toward credit intelligence represents a necessary evolution, not a technological luxury. Captives that embed AI-enabled, explainable, and human-in-the-loop underwriting frameworks will be better positioned to accelerate approvals, strengthen compliance, and enhance portfolio performance.

For captives building out their broader technology foundation, the whitepaper on the auto captive finance platform provides a strategic framework for what an AI-first, API-connected, and composable architecture looks like across the full captive technology stack, from origination through servicing.

This is where Check becomes a strategic enabler. By transforming traditional credit checks into intelligent, structured, and auditable decision workflows, Check helps captives modernize underwriting without disrupting their core systems. It empowers analysts with contextual insights, reduces manual workload, and ensures faster, more consistent, and governance-ready credit decisions.

To experience how NETSOL Check can operationalize intelligent, audit-ready underwriting within your existing ecosystem, book a demo today!

Related blogs

Blog

Turning trade-in friction into sales acceleration with Transcend Retail

Blog

From paper to signed: How Transcend Retail's eContracting closes deals faster

Blog