Blog

Beyond the verdict: Technology unlocking business agility and trust

By Jason Hurwitz Sales Director at NETSOL Europe,, on August 6, 2025

Navigate the post-ruling landscape with future-ready platforms and data-driven insights for smarter, faster and more ethical operations.

Table of Contents

Share this Blog:

The recent UK Supreme Court ruling narrows lender liability around undisclosed commissions, easing the threat of widespread compensation claims. While the ruling brought common sense to the commercial relationships in lending, it keeps the spotlight on appropriate commission arrangements. The FCA signalled that consumer redress, regulatory reform, market transparency and increased choice will be central to their next steps.

The role of technology

Technology is playing a transformative role in helping the UK finance industry remain agile, nimble and future-ready. Here’s how:

Highly configurable platforms

Legacy tech is slow and expensive to change. Modern, modular cloud platforms empower lenders to adapt swiftly to a changing landscape, helping them manage risk and seize opportunities.

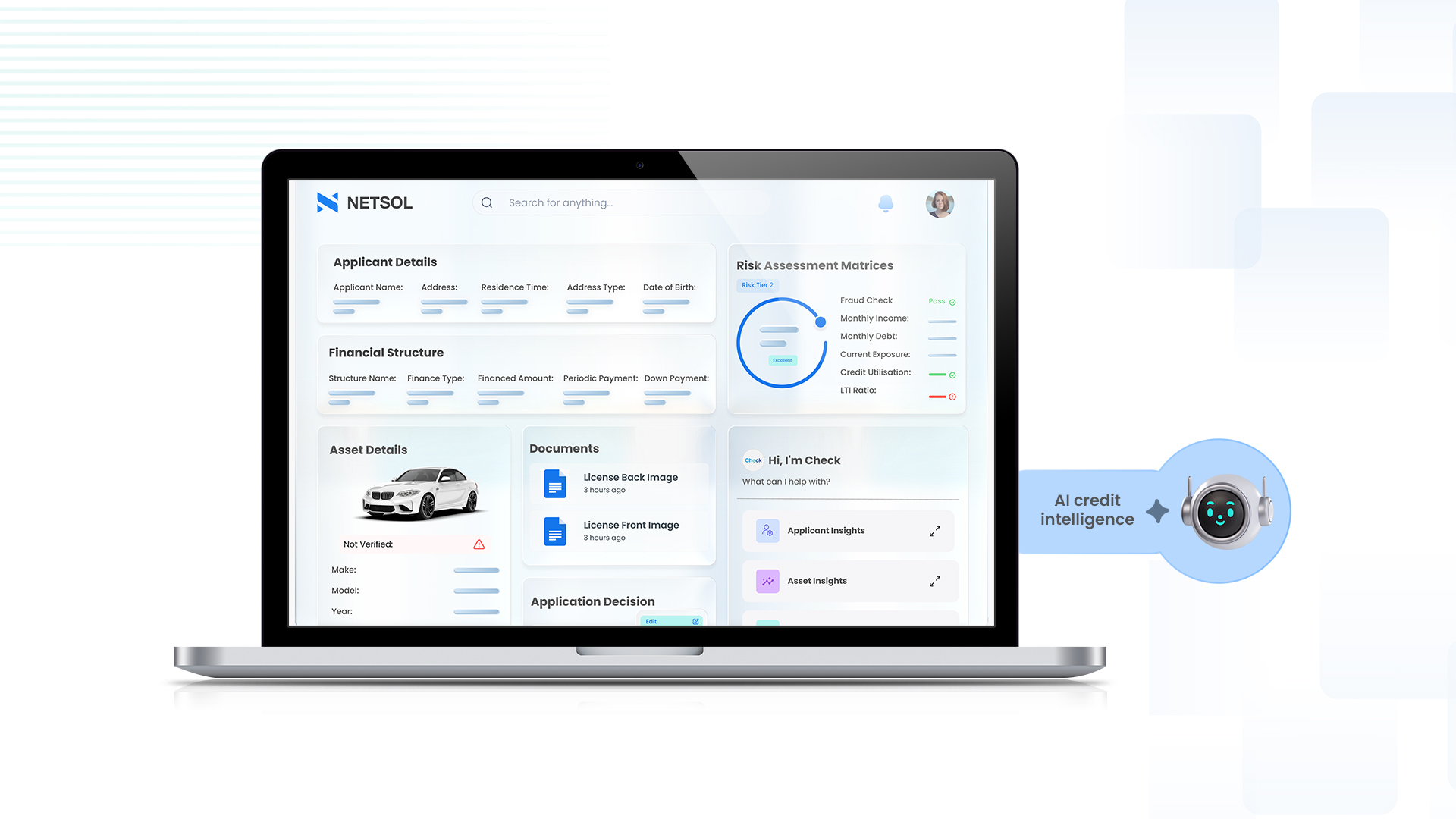

Artificial Intelligence

AI can play a critical role in helping car finance providers rebuild trust and ensure compliance. From automating affordability checks to enhancing transparency in decision-making, AI-driven solutions enable lenders to respond quickly to regulatory shifts while delivering fairer, more consistent customer outcomes.

Consumer duty and vulnerable customers: AI-driven analytics can identify vulnerable customers and tailor communications to meet regulatory expectations.

Trust-building: Generative AI chatbots and virtual assistants improve customer service, help inform the customer and provide transparency in financial advice.

Regulatory compliance: Machine learning helps firms monitor transactions and flag suspicious activity, improving anti-money laundering (AML) and fraud detection.

Smart system architecture

Digital-first approach: A digital-first approach brings choice direct to the consumer in a comfortable place of their choosing. Technology can allow the customer to configure the assets they need and build accompanying financing options at their home or office at a time of their convenience. This also empowers the customer to make more informed decisions about their purchases.

Integration: Smart ‘API-first’ functionality enables the seamless integration of choice and the bringing in of relevant additional services. This allows the tailor-making of bundled finance packages created to suit individual needs which can then be communicated in an easy to understand format

Seamless collection of data: Secure digital tools are available to bring in relevant identity and affordability data into the documentation and decision-making processes. This again allows customers to send information from a comfortable start point directly to the parties that need it.

Digital transformation

Car finance providers must track, audit and disclose every deal detail in real-time to build and maintain trust. Digital infrastructure isn’t just for today’s standards – it’s a strategic tool for futureproofing against evolving regulation. As regulatory expectations grow, firms must evidence accountability and ethical decision-making. Transparent digital systems are becoming standard rather than optional.

Going beyond

Although the ruling relieves immediate litigation pressure, it highlights the need for rigorous documentation and structured commission disclosure, which are here to stay. Brokers and lenders must now go beyond surface-level compliance to demonstrate genuine accountability and value.

NETSOL’s positioning

NETSOL’s solutions support this shift with features such as highly adaptable direct-to-customer portals, automated consent, transparent commission data and real-time audit trails. These tools enable brokers and lenders to meet rising regulatory demands in hours not weeks, while strengthening transparency and customer trust.

Related blogs

Blog

Australia’s asset finance outlook for 2026: Why agility will define the leaders

Blog

Four in five asset finance leaders want to integrate AI – but nearly half of IT budgets are stuck maintaining legacy systems

Blog